You may have signed papers or lost a job, but the bills didn’t pause. If your savings are thin or gone, every payment choice carries more weight, and even basic admin can feel harder than it should. This week’s job is simple: stop further damage, cover essentials first, and create a little breathing room.

In this article

- The first 72 hours: stop the financial bleeding

- What a bare-minimum budget actually looks like for the next 30 days

- The bills that matter first, and the ones that can wait a beat

- Income triage beats deeper cuts when the math still does not work

- The calls that can buy you time this week

- The four numbers worth tracking for the next 30 days

- Shared accounts, joint debt, and paperwork after separation need attention early

- Where most recovery plans fall apart

- A one-page reset for the next 30 days

- The moment to bring in outside help

The first 72 hours: stop the financial bleeding

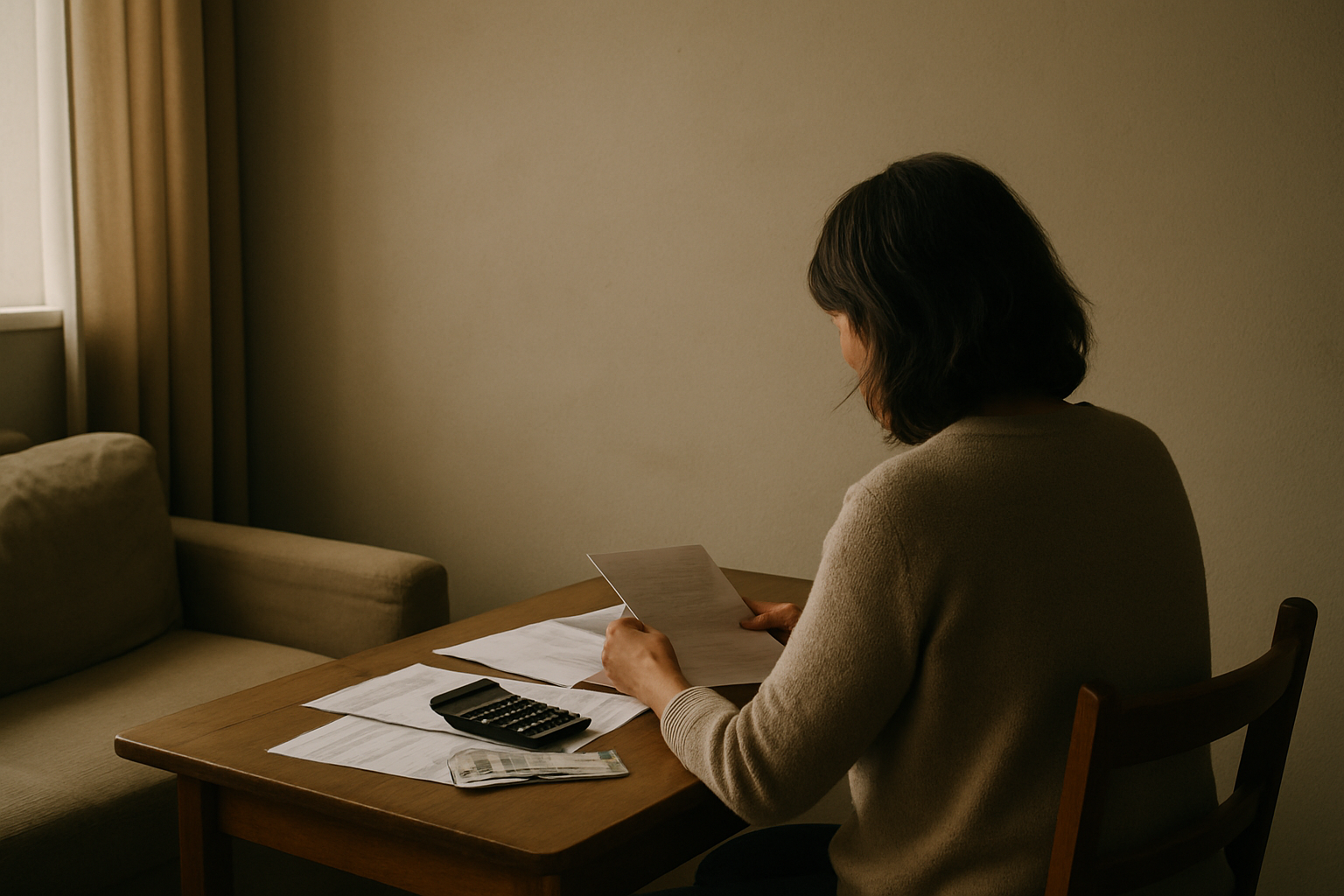

For the next three days, freeze optional spending. No takeout, no browsing purchases, no “small” digital extras, no adding anything to a cart unless it clearly keeps you housed, fed, insured, able to work, or able to care for your children. The goal is to stop money leaking out while you get a clear picture. A short freeze is easier to stick to than an open-ended promise to spend less forever.

Then pull the last 30 to 60 days of activity from every bank account, credit card, and payment app you use. If you have online access, this usually takes about 30 to 90 minutes. If you don’t, it may take longer because you’ll need to call for balances or request paper records. Look at actual transactions, not memory. Bank apps, Apple Wallet, Google Pay, PayPal, Venmo, and card statements often show recurring charges you stopped noticing.

Next, write down only the bills due in the next 14 days. Keep the list tight: housing, utilities, food, transport, insurance, debt minimums, childcare, phone, internet if you need it for work or a job search, and medicines. Don’t build a full monthly plan yet. Clear the next two weeks first, then plan the rest.

If your income has dropped, turn off automatic transfers and cancel or pause nonessential subscriptions the same day. This step often fails because people leave “small” recurring charges untouched: a streaming service, iCloud+, a fitness app renewing quietly through the App Store. Small charges matter when your margin is gone. Doing this yourself is free and usually takes one to two hours.

What a bare-minimum budget actually looks like for the next 30 days

Your goal for the next month is a survival budget, not a clean lifestyle reset or a perfect spreadsheet. You’re trying to keep the basics working long enough to think clearly again. Usually that means sorting every expense into three groups: must be paid this month, can be reduced, and can pause for 30 days. Rent sits in one group. A premium phone plan may sit in another. A gym membership, extra streaming services, and routine online shopping often belong in the third. Protecting Your Credit Score… looks at this specific angle in depth.

This can feel harsh after divorce or job loss because money decisions are carrying grief, anger, fear, or exhaustion with them. People often spend to self-soothe right when they can least afford to. That doesn’t make you careless; it means your budget needs to be temporary and specific enough to hold up in real life.

The better target is one workable month, not a heroic year-long reset.

Aim for one month of stripped-down decisions instead of making promises about the next year.

One common failure point is timing. People set a monthly total and forget that cash arrives and leaves weekly. If rent hits on the first, childcare hits on Monday, and income doesn’t arrive until Friday, your monthly budget may look fine while your bank balance still runs short midweek. For the next 30 days, watch cash timing as closely as total spending.

The bills that matter first, and the ones that can wait a beat

Put housing at the top of the list

Rent or mortgage payments usually come first because missing them can create fast-moving problems. Right after housing, pay utilities that affect safety or habitability: electricity, heat, water, or anything else that keeps the home usable. If you own a car you need for work or childcare, missing that payment may carry bigger consequences than the balance alone suggests.

Protect the costs that protect income

After shelter and core utilities, focus on the bills that keep you able to earn or look for work: transport, your phone, internet if you need it, and childcare if that’s what makes work possible. A cheaper month isn’t really cheaper if it means you can’t get to a shift or answer an employer’s call. It just pushes the problem into next week.

Be careful with insurance and medical costs

When cash is tight, insurance is often tempting to cut. Sometimes keeping coverage matters more than holding onto cash, because one lapse can create a much bigger problem later. For many people, that includes health insurance, car insurance required by law or needed to drive to work, and medicines, though it depends on your situation and local rules. Check the current terms before you skip any premium, because grace periods, reinstatement rules, fees, and coverage gaps vary.

Unsecured debts and memberships come after essentials

Credit cards, personal loans without collateral, and nonessential memberships usually come after core living costs. What matters is the consequence of missing a bill, not pride or balance size. A smaller bill with a severe penalty may need attention before a larger one with more flexibility.

Ranking bills by interest rate alone is often overrated during a crisis month; cash-flow damage matters more first.

Ranking your bills usually takes about 30 minutes. Fees and penalties depend on each account, so check the current terms before you decide to delay anything.

Income triage beats deeper cuts when the math still does not work

If your essential costs already exceed the income you’re likely to receive this month, more cutting probably won’t fix it. That’s the point where income triage matters more than trying to shave a little more off groceries or toiletries.

Fast income options to assess this week include extra shifts if they’re available, temporary work with short onboarding, selling unused items locally, asking for money someone already owes you, taking freelance or admin tasks you can finish quickly, or changing how adults in the household contribute to shared costs. Facebook Marketplace and eBay can turn clutter into cash faster than many formal side-income plans, though you may have to accept a lower sale price if you need money quickly. Task-based work can help if you already have transport and flexible hours. If applications and approvals take weeks, it’s probably too slow for the problem in front of you.

There are trade-offs. Quick cash can cost time, energy, childcare coordination, transport money, or emotional bandwidth you may not have much of right now. Selling essentials can create a new problem later if you have to replace them at a higher cost. Be especially careful about selling a car you need for work or tools you use to earn.

This advice often falls apart when people build rescue plans around income that hasn’t actually started yet. “I’ll drive this weekend,” “I’ll get a temp role soon,” or “a client might pay next week” aren’t real inflows until they’re scheduled and likely enough to count.

The calls that can buy you time this week

Call before you miss payments if you can. Landlords, utility companies, insurers, lenders, phone providers, medical offices, and other service providers sometimes offer hardship procedures, due-date changes, payment plans, fee waivers, or short pauses. What’s available depends on the account and your location. You don’t need a perfect story. You need to find out what options exist before fees stack up or the account moves into collections. We’ve since covered this in more detail in How to Stay Organized….

A simple script works best: “My income changed because of divorce/job loss. I can pay X by Y date. What hardship options do you have?” Keep the amount and date realistic. If they give you a few options, ask what changes under each one: the due date, any fees, your reporting status, whether service stays on, what it could cost later, and whether interest or penalties keep building during the arrangement. Take notes on every call so you’re not relying on memory afterward.

A lot of people put this off because it feels exposing. You may already feel judged by the situation and dread hearing “no.” Still these calls are often where you buy a little time. They cost nothing to make, though you should expect hold times and more than one conversation.

The four numbers worth tracking for the next 30 days

Cash on hand today

This is the money you can use right now across checking, savings you can access immediately without causing new problems, and any physical cash.

Money due in the next seven days

Seven days keeps your focus on timing instead of vague monthly totals. Include due dates and the minimum amounts needed to avoid immediate damage where that matters.

Essential weekly burn rate

Work out what it takes each week to keep housing-related bills moving, food coming in, transport working, your phone connected, and other essentials active. In a crisis month, a weekly number is easier to control than a broad monthly estimate.

Confirmed income arriving and when

Only count money that’s scheduled and likely: wages already due, support payments already ordered and expected on a known date if that applies to you, benefits already approved if relevant where you live, or sale proceeds that are effectively committed. These four numbers matter more right now than net worth snapshots or annual goals because they tell you whether this week works. Track them on paper, in your Notes app, or in a spreadsheet for about 10 minutes a day. How to Rebuild an… looks at this specific angle in depth.

Shared accounts, joint debt, and paperwork after separation need attention early

If divorce or separation is part of your rupture, review joint checking accounts, credit cards with authorized users or joint holders, autopay settings, beneficiaries where relevant, passwords, mailing addresses, and account recovery details right away. The quiet admin details matter. A utility bill still tied to an old card or statements still going to the wrong address can turn into missed payments quickly.

Legal responsibility and practical payment responsibility aren’t always the same after separation. An agreement between two people about who will pay a bill doesn’t always change what the lender or card issuer can still pursue if the account remains joint. That gap is where damage often starts.

This depends heavily on your situation. If there’s joint debt, a house, support obligations, retirement accounts being split, tax questions tied to filing status or support payments, contested assets, or unclear legal orders, bring in qualified help instead of guessing. Depending on what’s involved, that may mean a lawyer, mediator, accountant familiar with divorce issues in your area, or another properly qualified financial professional. Move too slowly and you leave room for unauthorized spending or missed obligations; move too fast without checking the legal implications and you can create a different set of problems.

Where most recovery plans fall apart

Shame-based avoidance is a big one. People stop opening mail, stop checking balances, send calls to voicemail, and hope a calm day will show up before they have to deal with any of it. (Related follow-up: Healthy Habits When Your….)

Another common failure point is overcorrecting. You cut everything at once: no social spending, impossible grocery targets, unrealistic fuel assumptions, no room for one-off school costs or replacement toiletries. That kind of plan may last five days before rebound spending wipes out the effort because it was too tight to work.

Crisis months get distorted when one-time costs land on top of normal spending. Legal filing fees, moving costs, deposits, replacement furniture for a second-home setup, interview travel, or sudden child care changes don’t reflect a usual month. If you fold them into regular spending instead of labeling them separately, your plan gets confusing fast.

Irregular bills slip through too: annual subscriptions you missed during triage, car registration renewals where they apply, school expenses that show up at odd times of year, and insurance due on a schedule other than monthly. A lot of people also try to repair everything at once—catch up on debt, rebuild emergency savings right away, restart retirement contributions at previous levels if they had them before, and restore old routines in the same month.

Recovery usually works better in stages. Most people should not rush to restart every old financial goal in the first recovery month.

A one-page reset for the next 30 days

Take one sheet of paper or one phone note and write only five lines: cash today; income dates; essential bills by due date; hardship calls to make; one income action for this week. Keep it where you’ll see it. A note on the fridge works. So does a pinned note on your phone if that’s what you’ll actually check.

Set one weekly check-in time for 20 minutes. Sunday evening works for some people. Friday lunch works better for others because they can act before weekends complicate things. During that check-in update only those five lines and decide whether any bill ranking has changed.

Pick one spending rule for this month that limits damage without asking for perfect discipline. A 24-hour wait before any nonessential purchase is a good example because it slows emotional spending without pretending emotion will disappear. Setting it up is free and usually takes 30 to 45 minutes. How to Create a… looks at this specific angle in depth.

The moment to bring in outside help

If you can’t cover housing, food, transport needed for work, or medicine even after cuts and hardship calls, bring in outside help now instead of waiting for things to get worse.

The same goes if you’re facing eviction proceedings, foreclosure risk, repossession risk on something essential to your income or family logistics where that applies in your jurisdiction, utility shutoff notices affecting habitability or safety rights in your area, wage problems with an employer such as missing pay you believe you’re owed under local law, or debt collection escalation you don’t know how to handle. We break this down further in What Bills Should You….

Divorce-related finances often need real professional input when legal orders are involved, taxes shift with filing status changes, support payments affect cash flow, property division is disputed, or retirement accounts are being divided under rules specific to your area and plan type. And if emotions are making basic money tasks impossible at all—opening statements, making calls, paying priority bills, ask one trusted person to sit with you for 30 minutes today while you make the first two calls.

Open your bank app now and write down these two numbers on paper: cash on hand today and bills due in the next seven days.

Quick answers to common questions

How do I prioritize bills when my income suddenly drops after a divorce or job loss?

Start with the bills that keep you safe, housed, and able to work: rent or mortgage, utilities, food, insurance, transportation, and any child-related essentials. After that, contact every other creditor before you miss a payment and ask for hardship options, lower minimums, or temporary pauses. Ignore the urge to pay everything evenly just to feel fair—right now, keeping your basics covered matters more than keeping every account perfectly current.

What should I do first if I have no emergency fund at all?

Make a bare-bones budget today and cut spending down to the essentials so you can stop the bleeding fast.

Should I use credit cards to get through this period?

Only if it's the difference between keeping the lights on and falling behind on essentials, and even then, use them carefully. Put necessities first, avoid using credit for nonessential spending, and know your limit before the balance starts growing faster than you can manage. If you do use a card, treat it as a short-term bridge while you work on income, payment plans, or other relief options.

How can I rebuild financially when I feel too overwhelmed to even start?

Pick one small move for today: list your bills, apply for one job, call one lender, or open a separate account for essentials. Tiny actions count because they turn panic into a plan, and a plan gives you back some control. You do not need to fix everything this week—you just need to make the next smart move and then the one after that.